.png)

When the stock market becomes volatile, one question always seems to come up: "Should I wait until things settle down before investing?"

It's a completely understandable concern. Watching the market swing up and down can be uncomfortable, especially if you're nearing retirement or relying on your investments to support your future income.

The problem is that the market never sends an announcement saying, "It's safe to invest again." By the time things feel comfortable, much of the recovery has often already happened.

Many people think market timing is simply knowing when to sell.

In reality, it requires getting two difficult decisions exactly right:

Miss either one, and your long-term returns can suffer. That's what makes market timing so difficult, even for professional investors.

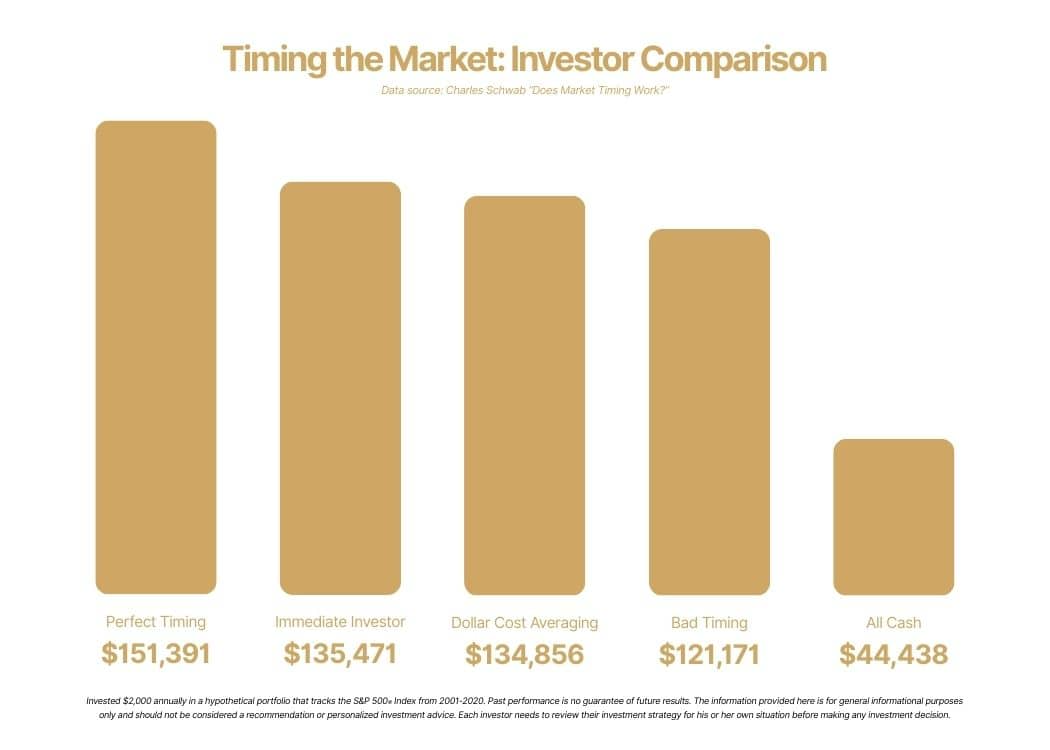

One of my favorite examples comes from a Charles Schwab study.

The study followed five hypothetical investors over a 20-year period (2000–2020). Each investor received $2,000 at the beginning of every year to invest, but each followed a different strategy.

The results were eye-opening.

As expected, the investor with perfect timing finished with the highest account value. But that's not the surprising part.

The investor who simply invested the money immediately each year finished very close to the perfect market timer. The investor who invested monthly also produced strong long-term results.

The investor who finished far behind everyone else?

The one who continually waited in cash, convinced a better buying opportunity was just around the corner.

The lesson isn't that market declines don't matter, they certainly do.

The lesson is that trying to perfectly predict them is incredibly difficult, and sitting on the sidelines often carries its own risk.

Successful investing isn't about being perfect. It's about consistently putting your money to work and allowing compounding to do what it does best over long periods of time.

Markets have experienced wars, recessions, political uncertainty, inflation, pandemics, and countless other events. Yet over the long run, they have historically continued to move higher despite periods of significant volatility.

This doesn't mean you should simply ignore risk.

As retirement approaches, your investment strategy should evolve. Someone who is five years from retirement shouldn't necessarily have the same portfolio as someone who is 30 years away.

That's why we spend so much time helping clients build retirement income plans that are designed to weather market volatility. The goal isn't to eliminate every downturn (that's impossible). The goal is to structure your retirement so market swings don't force you into making emotional decisions at the worst possible time.

A well-designed retirement plan includes more than just investments. It considers your income needs, cash reserves, tax strategy, Social Security timing, and other sources of retirement income so you're prepared regardless of what the market is doing.

Instead of asking: "Should I get out of the market?"

Consider asking: "Is my retirement plan built to handle market ups and downs?"

That's a much more productive conversation.

The best investment strategy isn't about perfectly timing the market. It's about having a thoughtful, long-term plan- and the confidence to stick with it when headlines become noisy.

While buying during a market downturn can be beneficial, consistently predicting when those downturns will occur is extremely difficult. Waiting for the "perfect" opportunity often means missing periods of recovery and long-term growth.

It depends on your situation. If you have a lump sum available, investing it immediately has historically outperformed spreading it out over time more often than not. However, dollar-cost averaging can reduce the emotional stress of investing during volatile markets and may help some investors stay disciplined. The right strategy depends on your financial goals and comfort with risk.

If retirement is only a few years away, your focus shouldn't be on trying to time the market. Instead, your investment strategy should be designed to provide the income you'll need while protecting a portion of your savings from short-term market declines. A balanced retirement income plan can help reduce the impact of market volatility.

Moving entirely to cash may feel safer, but it creates another challenge- deciding when to reinvest. Missing just a handful of the market's strongest recovery days can significantly reduce your long-term returns. Before making major investment changes, it's important to evaluate whether your overall retirement plan still aligns with your goals.

One of the most common mistakes is making emotional decisions based on fear or headlines. Successful investors typically focus on their long-term plan rather than reacting to short-term market movements.

If recent market volatility has you questioning whether your current investment strategy is still appropriate, we'd be happy to help you evaluate your retirement plan and determine whether it's positioned for both today's uncertainty and tomorrow's opportunities.

Ethan Ball, CRPC®

Financial Advisors in Cedar Rapids, IA

Helping you create a stress-free, simplified retirement

Investment advisory services are offered through Fusion Capital Management, an SEC registered investment advisor. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration is not an endorsement of the firm by the commission and does not mean that the advisor has attained a specific level of skill or ability. All investment strategies have the potential for profit or loss.